The Latest

Why Now Is The Time To Invest In AI Applications

It is our thesis that the best investment opportunity in AI has shifted from foundation models to the application layer, software that packages model capability into complete workflows, owning user interface, decision logic, integrations, and system-of-record adjacency, rather than simply exposing model access.

Raw model access alone does not solve an enterprise problem, and in many of the most valuable verticals it is not a viable option. When employees paste patient records, contracts, or financial data into a general-purpose LLM, that data leaves the organization's control, potentially violating HIPAA, attorney-client privilege, FINRA rules, or internal data governance policies. In healthcare, legal, insurance, and finance, this is not just a theoretical risk but actually structural disqualifier.

Beyond compliance, general-purpose AI places the integration burden on the employee: users must know what to ask, how to structure prompts, and what to do with unformatted output. Enterprise applications invert this entirely. The AI is embedded directly into the workflow, connected to systems of record, operating within the organization's compliance perimeter, and trained on domain-specific data a general chatbot will never see. In healthcare, for example, leading applications automatically transfer notes into the EHR, verifies output against clinical guidelines, and maintains audit trails all within a governed environment.

Beyond compliance, general-purpose AI places the integration burden on the employee: users must know what to ask, how to structure prompts, and what to do with unformatted output. Enterprise applications invert this entirely. The AI is embedded directly into the workflow, connected to systems of record, operating within the organization's compliance perimeter, and trained on domain-specific data a general chatbot will never see. In healthcare, for example, leading applications automatically transfer notes into the EHR, verifies output against clinical guidelines, and maintains audit trails all within a governed environment.

Model capability is now strong enough, inference economics are improving rapidly, and enterprise adoption is broad enough that the next wave of value creation will come from companies that convert raw intelligence into workflow, compliance, distribution, and measurable ROI. The winning AI companies will not merely expose model access, they will become the operating systems for specific jobs and industries. This shift is being further accelerated by agentic AI: systems that take sequences of autonomous actions rather than simply responding to prompts, which deepens workflow lock-in for application companies that move early.

Three Key Market Drivers

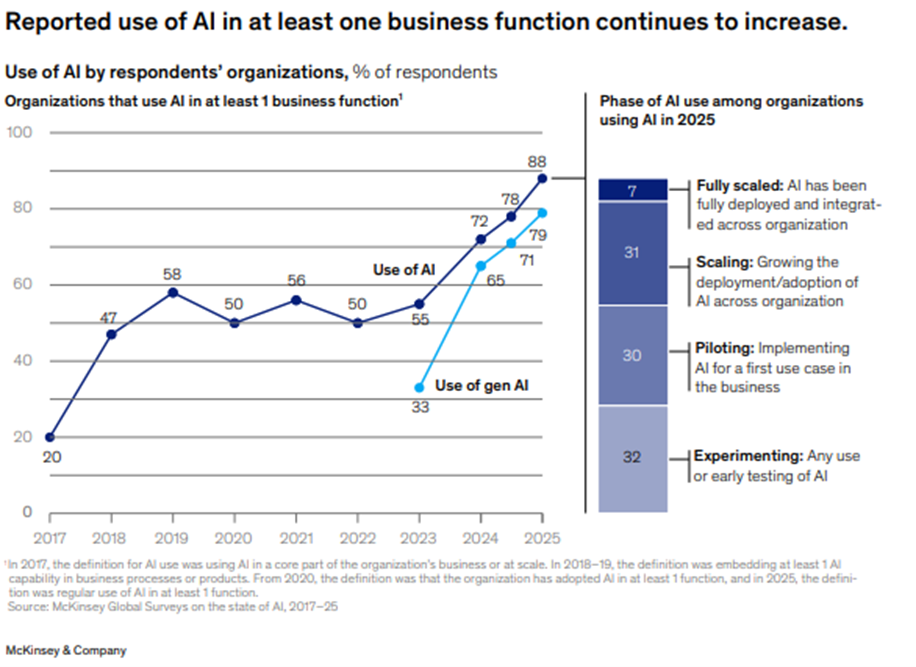

Adoption is broad, but scaling is still early. McKinsey reports that “nearly nine out of ten organizations are regularly using AI”, yet most have not embedded it deeply enough into workflows to realize full enterprise value. Nearly two-thirds have not yet begun scaling AI across the enterprise. Deloitte similarly reports that worker access to AI rose 50% in 2025 and that the number of companies with 40% of AI projects in production is expected to double within six months. That combination—high usage but incomplete deployment—creates a compelling setup for application-layer winners.

Unit economics are improving fast enough to support durable software businesses. Stanford’s 2025 AI Index reports that inference cost for a GPT-3.5-level system fell more than 280-fold between November 2022 and October 2024. At the hardware level, costs declined 30% annually while energy efficiency improved 40% each year. Falling model costs expand gross-margin headroom for application companies and allow pricing to be anchored to workflow value rather than raw compute.

Market leaders are already separating from the field. This is no longer a theoretical market. The strongest application businesses exhibit enterprise SaaS characteristics: high ACV, multi-year contracts, expansion through seat or workflow growth, and improving gross margins as inference costs decline relative to pricing.

Top Risks

Model commoditization. Applications that do not own workflow, proprietary data, integration depth, or compliance may see margin pressure as core model access becomes cheaper and more interchangeable.

Regulated-domain trust risk. Healthcare, legal, insurance, and finance industries offer large budgets but also highly regulated imposing high standards around hallucinations, auditability, privacy, and explainability. While these standards structurally disqualify general-purpose LLMs in these markets, they create a compliance-driven moat for applications that meet these standards.

Uneven enterprise scaling. Many customers are still in pilot mode. Some markets may scale more slowly than headline AI enthusiasm suggests, so investments should favor products with clear ROI, budget ownership, and high-frequency usage.

Incumbent platform encroachment. Microsoft Copilot, Salesforce Einstein, Google Workspace AI, and ServiceNow are embedding AI natively into tools enterprises already license and trust. Standalone application companies without deep vertical moats, proprietary data advantages, or regulated-domain expertise face genuine risk of margin compression as platform incumbents expand into adjacent workflows. Horizontal platforms will capture generic productivity use cases, but vertical applications win where domain-specific data, compliance requirements, and workflow depth exceed the capabilities of generalized copilots

What Winners Have in Common

The application companies that appear most durable share several characteristics: (1) they operate in regulated or high-stakes domains where trust, auditability, and compliance create natural barriers to entry; (2) they accumulate proprietary data that improves model performance in ways competitors cannot replicate without equivalent workflow access that compound with use; (3) they are embedded in daily, high-frequency workflows rather than occasional tasks; (4) they own the budget line directly rather than competing as a feature inside a larger suite; and (5) they have meaningful integrations with existing enterprise systems (EHRs, practice management platforms, financial data providers) that raise switching costs. Companies with three or more of these attributes warrant the strongest conviction.

Where to Invest

The most attractive opportunities in AI applications are concentrated in vertical workflows where software directly impacts revenue, cost, or risk and where budgets are already established. These include areas such as healthcare revenue cycle and documentation, legal workflow automation, financial research, insurance claims, and industrial operations. Within these markets, the most compelling opportunities are companies embedded directly into core workflows and systems of record, where integration depth and daily usage drive both retention and data advantage.

Priority should be given to applications where value capture is tied to outcomes rather than usage. Pricing models linked to revenue uplift, cost savings, or workflow completion are more resilient as underlying model costs decline, allowing companies to sustain premium pricing and scale as durable, high-margin software businesses. AI applications targeting healthcare, legal, insurance, and finance industries should be prioritized.

Conclusion

The case for investing in AI applications is strongest now because the market has reached a rare transition point: adoption is proven, economics are improving, and category leaders are beginning to lock in customer workflows before markets fully consolidate. The next decade’s most valuable AI companies are likely to be the ones that translate model intelligence into indispensable software for specific jobs, industries, and decisions. The opportunity is timely because the potential winners are starting to emerge, but the window to back category leaders at reasonable valuations is narrowing.

Selected Sources

- Stanford HAI, 2025 AI Index Report: https://hai.stanford.edu/ai-index/2025-ai-index-report

- McKinsey, The State of AI: https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

- Deloitte, State of AI in the Enterprise: https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence/content/state-of-ai-in-the-enterprise.html

- Reuters on OpenEvidence valuation and adoption: https://www.reuters.com/business/healthcare-pharmaceuticals/medical-ai-startup-openevidence-doubles-valuation-12-billion-latest-round-2026-01-21/

- Harvey funding and usage metrics: https://www.harvey.ai/blog/harvey-raises-at-dollar11-billion-valuation-to-scale-agents-across-law-firms-and-enterprises

- Reuters on Abridge valuation and traction: https://www.reuters.com/business/healthcare-pharmaceuticals/healthcare-startup-abridge-raises-300-million-led-by-vc-firm-andreessen-horowitz-2025-06-24/

- Reuters on AlphaSense valuation and ARR: https://www.reuters.com/technology/alphasense-valued-4-bln-after-latest-funding-round-2024-06-11/

- EvenUp Series E announcement: https://www.evenuplaw.com/blog/evenup-2b-valuation/

This memo is provided for informational and discussion purposes only and does not constitute investment advice or an offer to buy or sell any security. The views expressed are based on publicly available information believed to be reliable as of the date of this memo, but no representation or warranty is made as to accuracy or completeness.

Private company valuations are based on latest publicly disclosed funding-round announcements or reputable reporting and may not reflect current fair market value.