The Latest

The Demographic Imperative: Why Robotics Is No Longer Optional

For most of the 20th century, the global economy operated on a demographic assumption that seemed as reliable as gravity: there would always be more people. The world rode a wave of explosive population growth that powered economic expansion, fueled consumer demand, and provided a deep, renewable reservoir of labor. That era is definitively ending.

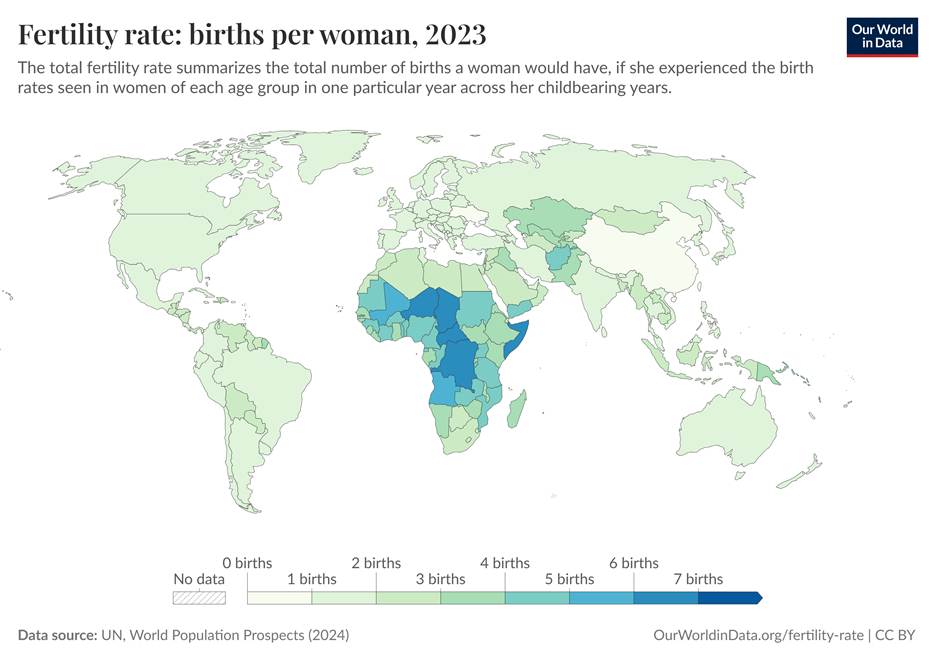

This is not a matter of speculation; it is a matter of arithmetic. Fertility rates are declining across virtually every developed economy, and increasingly in emerging ones too. The pivotal moment arrived quietly in 1960 with the introduction of the oral contraceptive, marking the beginning of a prolonged, structural fertility decline that has fundamentally altered the human trajectory. Birth rates have since fallen to below replacement levels across much of Europe, East Asia, and North America.

Today, the majority of the world's population lives in countries with fertility rates below the 2.1 replacement threshold necessary to maintain a stable population. The global demographic map has flipped: what was once a world of expanding populations (brown on the demographer's heatmap) is increasingly a world of shrinking ones (blue). We are entering an age where the primary constraint on growth is not capital, land, or technology, but people.

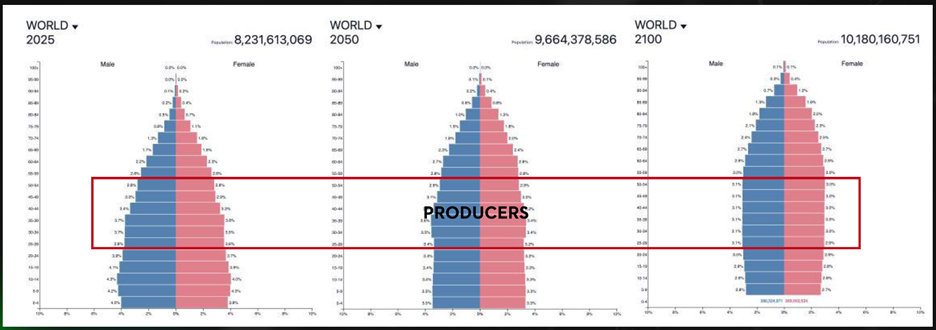

The Pyramid Has Inverted

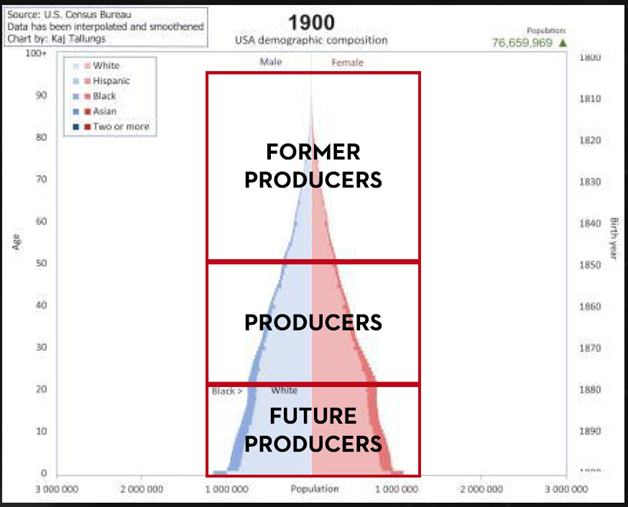

In 1900, the United States population pyramid was a true triangle, a broad, robust base of children and young adults (future and current producers), tapering gradually to a narrow apex of elderly dependents. That geometric shape was a machine for economic growth. It ensured that for every retired person consuming resources, there were multiple workers producing them.

By 2020, that pyramid had transformed into something closer to a column or an inverted triangle. The "producer" cohort, roughly ages 25 to 54, is increasingly squeezed between growing elderly populations above and shrinking youth populations below.

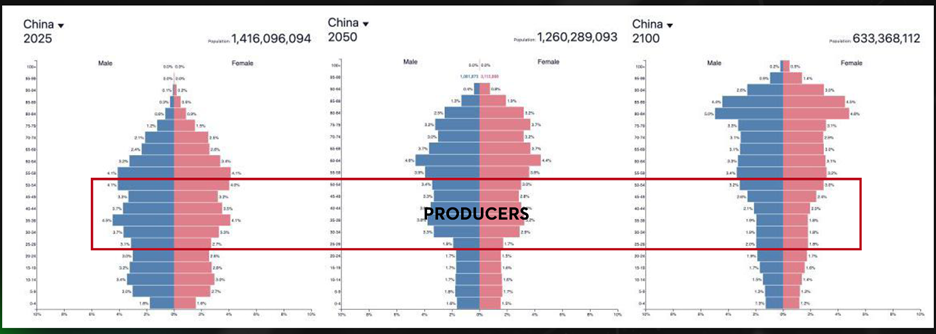

This is not uniquely American. The same story is playing out in China, which faces an extraordinary demographic contraction, from 1.4 billion people today projected down toward 633 million by 2100. It is happening in Germany, Japan, South Korea, and across virtually every major economy.

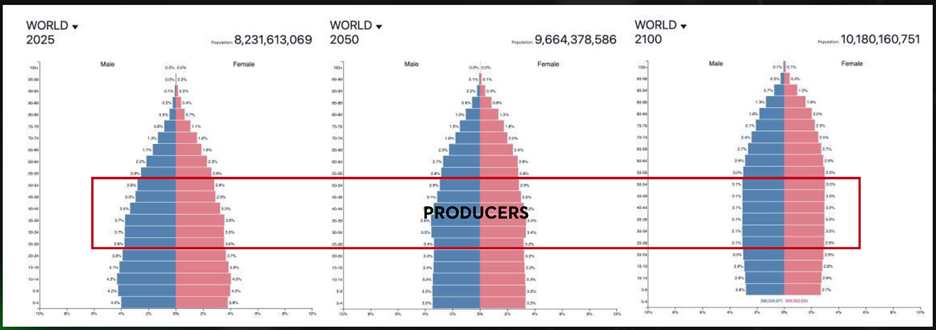

The implications are staggering. By 2050, the world will have more people aged 65 and older than ever before in history. By 2100, global population growth will have nearly flatlined. The surplus of labor that defined the industrial age has evaporated, replaced by a structural deficit that will define the rest of this century.

The implications are staggering. By 2050, the world will have more people aged 65 and older than ever before in history. By 2100, global population growth will have nearly flatlined. The surplus of labor that defined the industrial age has evaporated, replaced by a structural deficit that will define the rest of this century.

The Economic Consequence: Growth Without People

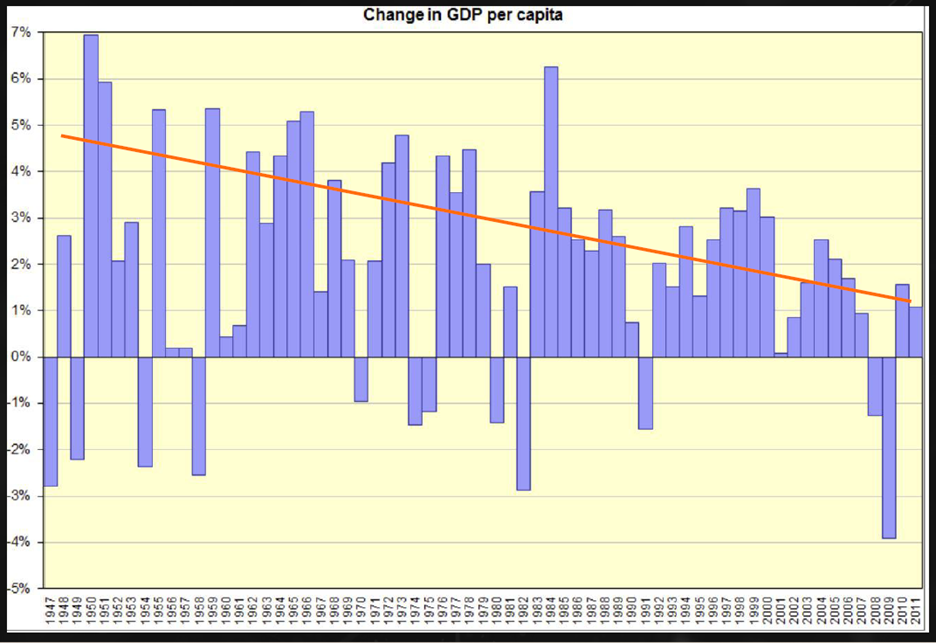

Population growth has historically been one of the most reliable engines of GDP growth. More workers mean more output. More young consumers mean more demand. When population growth stalls, so does the easy path to prosperity. The macroeconomic data bears this out: since the 1940s, annualized US GDP per capita growth has been on a long, slow downward trend, even amid periods of technological acceleration like the internet boom.

The world cannot grow its way to prosperity through demography alone anymore. The arithmetic no longer works. If the number of workers remains flat or declines, the only way to grow an economy, and more importantly, to maintain the social safety nets, healthcare systems, and living standards we have built, is to dramatically increase the value generated by every remaining hour of human labor.

"This is not a marginal efficiency gain. This is the mechanism by which civilization maintains its obligations to itself."

The Only Equation That Solves This

There is one variable that can compensate for fewer workers: productivity per worker. If the workforce shrinks by 20%, but the remaining workforce becomes 50% more productive, the math becomes survivable. If each producer can do the work of 1.5 or 2 people, through automation, robotics, and physical AI, then society can continue to function and flourish.

This is not a marginal efficiency gain; it is a civilizational necessity. Caring for aging populations, maintaining infrastructure, growing food, and delivering goods all require labor. If the labor pool shrinks, output per person must rise. Robotics and physical AI are the mechanism by which that productivity leap becomes possible.

We must decouple economic output from human headcount. In the past, automation was often framed as a threat to jobs. In the demographic reality of the 2030s and 2040s, automation will be the only thing keeping the lights on. It is the bridge that allows a smaller generation to support a larger one.

The State of the Technology, and the Opportunity Within the Gap

The good news is that robotics has graduated from the lab. Autonomous mobile robots (AMRs), collaborative robotic arms (cobots), AI powered logistics systems, and physical AI platforms are real, deployed, and generating return on investment in warehouses, hospitals, farms, and factories today. We are seeing machines that can navigate chaotic environments, handle delicate objects, and work safely alongside humans.

However, the honest caveat remains: the technology is not yet where it needs to be. Reliability, safety, adaptability, and cost per task still represent meaningful barriers to the kind of ubiquitous deployment the demographic picture demands. Most robots today are still too expensive, too brittle, or too difficult to program for general purpose use.

The gap between what robots can do today and what the world needs them to do represents one of the most important technology challenges of the next two decades, and one of the most compelling investment theses of our time. The capital that flows into closing this gap is not just chasing a market opportunity; it is funding the essential infrastructure of the future economy.

This is the moment. The demographic clock is ticking, slowly enough that it's easy to ignore in any given quarter, but fast enough that delay compounds its consequences exponentially. The companies solving the hard problems in physical AI and robotics: safety, adaptability, cost, and human and robot collaboration, are not building niche products. They are building the infrastructure for human civilization.

For investors and founders, the question is not whether the world will need more robots. It will. The question is who will build them, and who will be positioned when the urgency becomes impossible to defer. The prosperity of the next century will not be inherited. It will be engineered.